The Behavioral Liquidity Trap: When the Mind Gets Stuck (Behavioral Economy Series Part 6)

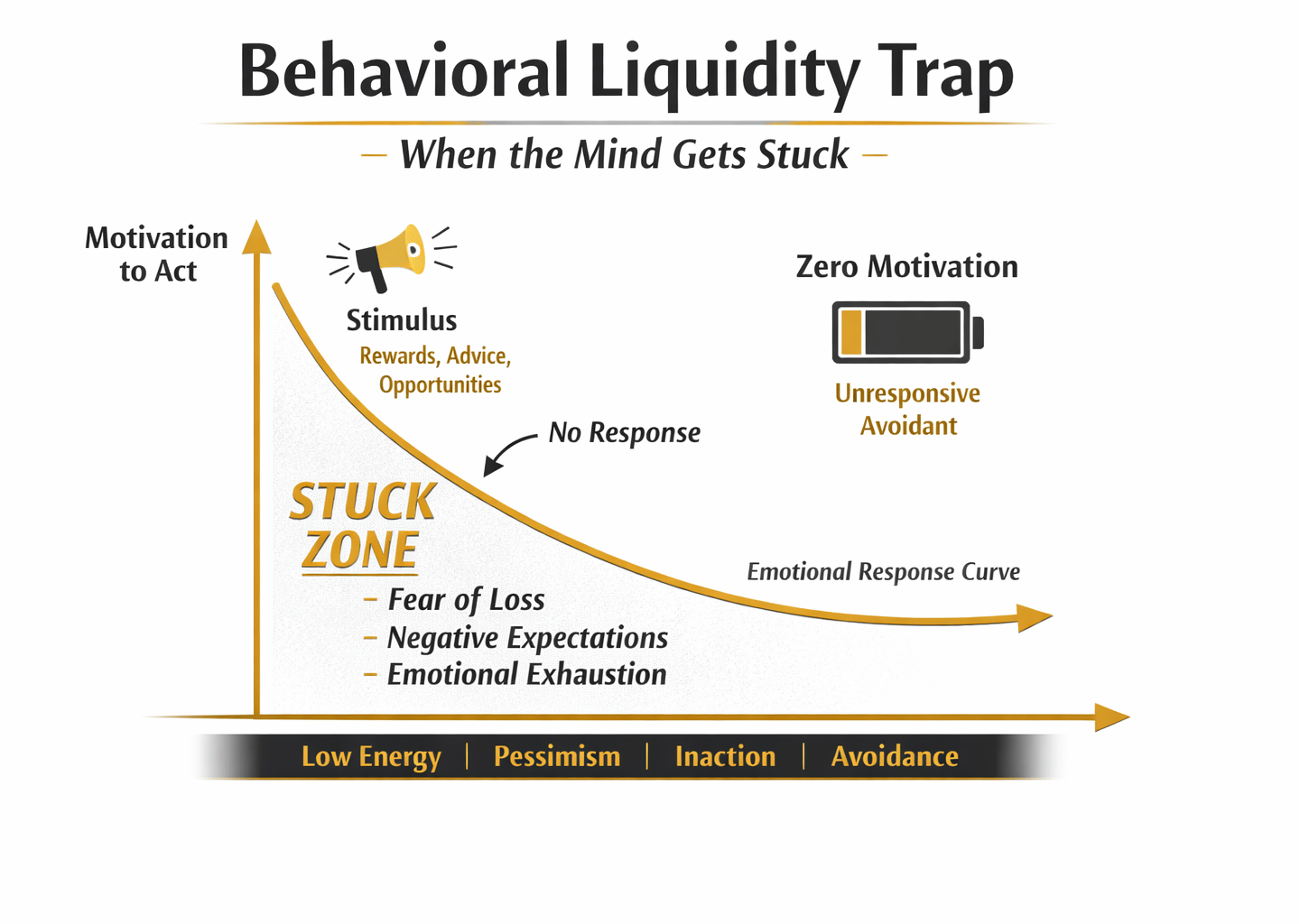

In economics, a liquidity trap happens when an economy becomes unresponsive to stimulus. Interest rates fall, money becomes cheap, opportunities exist — yet people refuse to spend or invest. They hold onto their cash because fear, uncertainty, and pessimism override every incentive to move. The system freezes, not because resources are absent, but because confidence has collapsed. The same thing happens inside the human mind. A behavioral liquidity trap is a psychological state where a person becomes emotionally and mentally “stuck.” They know what to do, they want to do it, and they may even have the skills to do it, but they cannot convert intention into action. Their internal motivation system becomes unresponsive, just like an economy that no longer reacts to monetary policy. This stuckness is not laziness, weakness, or lack of discipline. It is a breakdown in emotional liquidity, the psychological energy that allows us to take risks, make decisions, start tasks, and follow through. When emotional liquidity dries up, the mind begins to hoard its remaining energy the same way households hoard cash during a recession. Every action feels expensive. Every decision feels risky. Every step forward feels like a threat. People in this state often say things like: “I know exactly what I need to do, but I can’t get myself to start.” “I want to change, but something in me feels frozen.” “I’m tired before I even begin.” These are not character flaws, they are symptoms of a behavioral liquidity trap. Just as an economy becomes stuck when fear outweighs opportunity, the mind becomes stuck when emotional depletion, cognitive rigidity, and pessimistic expectations converge. The person loses the psychological flexibility to imagine alternatives, the energy to act on them, and the confidence to believe change is possible. The result is a closed loop: low emotional liquidity leads to inaction, inaction produces negative outcomes, negative outcomes reinforce pessimism, and pessimism drains emotional liquidity even further.

Enoma Ojo (2026)

6/20/202611 min read

Introduction: When the Economy Freezes, the Mind Freezes Too

In macroeconomics, a liquidity trap occurs when interest rates fall so low that monetary policy loses its power to stimulate spending. People hold on to cash rather than circulate it, even when borrowing is cheap and opportunities are abundant. The economy becomes psychologically paralyzed, not because resources are unavailable, but because fear, uncertainty, and pessimistic expectations override rational incentives (Krugman, 1998).

Human behavior follows the same pattern. There are moments when individuals become trapped in a psychological version of this phenomenon, a behavioral liquidity trap. Emotional energy stops circulating. Motivation collapses. The internal “interest rate” that normally encourages action, exploration, and risk‑taking falls to zero. Even when opportunities are present, the person cannot convert potential into movement.

This essay explores how emotional stagnation mirrors economic stagnation, why people struggle to “stimulate” change in their lives, and how behavioral economics helps explain the invisible forces that keep the mind stuck.

1. Liquidity Traps: A Brief Economic Analogy

Economists describe a liquidity trap as a condition where monetary policy becomes ineffective because people prefer to hoard money rather than spend or invest it (Keynes, 1936). Even if central banks lower interest rates to zero, households and firms remain unresponsive. The economy becomes inert.

Three psychological features define a liquidity trap:

1. Fear of loss outweighs potential gain

2. Expectations of the future become pessimistic

3. Agents prefer holding resources rather than deploying them

These same features appear in human behavior. When people enter a behavioral liquidity trap, they hoard emotional resources, energy, creativity, confidence, hope, instead of deploying them into meaningful action. They become risk‑averse, pessimistic, and immobilized. The mind, like the economy, becomes unresponsive to stimulus.

2. Emotional Liquidity: The Currency of Human Behavior

In behavioral economics, emotions are not irrational noise; they are part of the decision‑making architecture (Loewenstein, 2000). Emotions act as a form of psychological liquidity, enabling individuals to:

initiate action

sustain effort

tolerate uncertainty

pursue long‑term goals

recover from setbacks

When emotional liquidity is high, people feel capable of movement. They take risks, explore opportunities, and adapt to change. When emotional liquidity is low, even simple tasks feel overwhelming. Just as economies require circulating capital, humans require circulating emotional energy.

3. How Emotional Stagnation Mirrors Economic Stagnation

3.1 Hoarding Behavior

In a liquidity trap, households hoard cash because they fear future instability. In a behavioral liquidity trap, individuals hoard emotional energy for the same reason. They conserve effort, avoid commitments, and withdraw from challenges.

This is not laziness; it is psychological risk management.

Research shows that when people anticipate negative outcomes, they become more conservative in their decisions, even when the probability of loss is low (Kahneman & Tversky, 1979). The mind defaults to protection mode.

3.2 Diminished Responsiveness to Incentives

In economics, lowering interest rates is supposed to stimulate borrowing and spending. But in a liquidity trap, incentives lose their power.

Similarly, in a behavioral liquidity trap:

Encouragement does not motivate

opportunities do not excite

Advice does not translate into action

Deadlines do not create urgency

The system becomes unresponsive.

3.3 Expectations Collapse

Expectations shape economic behavior (Mankiw, 2019). When people believe the future will be worse, they stop investing. The same is true psychologically. When individuals expect failure, disappointment, or rejection, they stop investing in themselves. They stop applying for jobs, stop pursuing relationships, stop trying new things. The future becomes a self‑fulfilling prophecy.

4. Why People Struggle to “Stimulate” Change in Their Lives

4.1 Pushing on a String

Economists describe monetary policy in a liquidity trap as “pushing on a string.”, you can pull people toward spending, but you cannot push them into it.

Motivation works the same way. You can inspire, encourage, or equip them with tools, but you cannot push them into action if their internal system is frozen. Behavioral change requires internal liquidity, not external pressure.

4.2 The Weight of Cognitive Overload

When emotional liquidity is low, cognitive load increases. People become overwhelmed by decisions that normally feel manageable. Research shows that stress reduces working memory and narrows attention, making it harder to initiate change (Schmeichel & Baumeister, 2004). The mind becomes cluttered, and cluttered minds do not move.

4.3 Learned Helplessness

Repeated failure or prolonged stress can create a psychological state known as learned helplessness, the belief that effort does not matter (Seligman, 1975). This is the behavioral equivalent of economic stagnation.

When people believe nothing will change, they stop trying.

4.4 Loss Aversion Dominates

Loss aversion, the tendency to fear losses more than we value gains, becomes amplified in emotional stagnation (Kahneman & Tversky, 1979). People avoid change because:

“What if it gets worse?”

“What if I fail again?”

“What if I lose what little I have left?”

The fear of loss paralyzes the possibility of gain.

5. The Psychology of Stuckness: A Behavioral Model

A behavioral liquidity trap does not emerge from a single cause; it is the product of a convergence, a triad of forces that quietly erode the mind’s capacity for movement. Emotional depletion, cognitive rigidity, and expectational pessimism form a closed psychological circuit, each reinforcing the other until the individual’s internal economy collapses into inertia. What begins as fatigue becomes paralysis; what begins as caution becomes avoidance; what begins as doubt becomes despair. The result is a deflationary spiral of the psyche, a state where emotional liquidity drains away and the mind ceases to circulate energy, ideas, or hope.

Emotional depletion is the first and most visible symptom. It is the exhaustion that follows prolonged effort without reward, the fatigue that accumulates when one’s psychological reserves are spent faster than they are replenished. In economic terms, it is the equivalent of a liquidity shortage; the system still exists, but it lacks the liquidity necessary for exchange. When emotional energy runs low, even simple actions feel costly. The person begins to ration effort, conserving what little vitality remains. They withdraw from challenges, delay decisions, and avoid risks, not because they lack desire, but because the cost of movement feels unbearable. Emotional depletion transforms ambition into hesitation and turns the ordinary friction of life into a wall.

Cognitive rigidity deepens the trap. As emotional liquidity declines, the mind loses flexibility, its ability to imagine alternatives, generate creative solutions, or reframe problems. The person becomes locked into repetitive thought patterns, circling the same conclusions without escape. This rigidity mirrors the economic phenomenon of structural stagnation: when an economy cannot adapt to new conditions, innovation stalls, and recovery slows. Psychologically, rigidity manifests as tunnel vision, the inability to see beyond current constraints. The individual becomes trapped in habitual reasoning, unable to conceive of new strategies or possibilities. The mind’s elasticity, once a source of resilience, hardens into a fixed structure that resists change.

Expectational pessimism completes the triad. When emotional energy is depleted and cognitive flexibility collapses, the future begins to look threatening rather than promising. The person anticipates failure before it occurs, interpreting every uncertainty as danger. In behavioral economics, expectations drive investment; when expectations fall, spending contracts. Similarly, when psychological expectations deteriorate, motivation contracts. The person stops investing in themselves, in relationships, goals, or growth, because the anticipated return feels negative. Hope becomes a liability. The future, once a field of possibility, becomes a mirror of fear. Together, these forces create a closed loop, a self‑reinforcing cycle that sustains the behavioral liquidity trap. Low emotional liquidity leads to reduced action; reduced action produces negative outcomes; negative outcomes reinforce pessimism; pessimism further drains emotional liquidity. The system feeds on itself. Each component amplifies the others, creating a feedback loop of stagnation. The more the person withdraws, the more depleted they become; the more depleted they become, the less capable they are of imagining alternatives; the less they imagine, the more hopeless the future appears. The cycle continues until the psychological economy reaches zero movement, a state of emotional deflation.

This deflationary spiral is not merely metaphorical. It reflects measurable patterns in human behavior and cognition. Studies on learned helplessness (Seligman, 1975) show that repeated exposure to uncontrollable stressors leads individuals to stop attempting change, even when opportunities arise. Research on cognitive rigidity (Beck, 2011) demonstrates that depressive thought patterns narrow perception and inhibit problem‑solving. And emotional exhaustion, documented in burnout literature (Maslach & Leiter, 2016), reduces motivation and impairs decision‑making. Each of these findings corresponds to one component of the behavioral liquidity trap: depletion, rigidity, and pessimism, they describe a system that mirrors economic stagnation with striking precision. In this state, external stimulus, advice, encouragement, and opportunity function like monetary policy in a liquidity trap: it loses effectiveness. The person hears motivational words but cannot convert them into action. They receive opportunities but cannot respond. The psychological “interest rate” has fallen to zero. The usual levers of change, discipline, planning, and inspiration fail to generate movement because the underlying liquidity is gone. The system is not broken; it is frozen.

Recovery begins not with pressure but with circulation. Just as economies escape liquidity traps through small injections of confidence and gradual restoration of flow, individuals escape behavioral traps through micro‑movements, small, low‑risk actions that rebuild emotional liquidity. Each act of engagement, no matter how minor, reintroduces motion into the system. Over time, these micro‑movements accumulate into momentum. Emotional energy replenishes, cognitive flexibility returns, and expectations begin to shift. The deflationary spiral reverses. The behavioral liquidity trap, therefore, is not a failure of willpower but a failure of circulation. It reveals how deeply human functioning depends on the flow of emotional and cognitive resources. When that flow stops, the mind behaves like an economy in recession, conserving, contracting, and waiting for confidence to return. Understanding this dynamic reframes stagnation not as weakness but as a systemic condition, one that requires stimulus, patience, and renewal rather than judgment.

6. Why Traditional Motivation Fails and How the Mind Recovers

Traditional motivation often assumes that people possess enough emotional liquidity to act on new information. It presumes that if individuals are given the right advice, inspiration, or discipline, they will naturally convert intention into movement. Yet, in the behavioral liquidity trap, this assumption collapses. The problem is not knowledge, desire, or discipline; it is liquidity itself, the psychological capacity to transform intention into action. When emotional liquidity dries up, the mind becomes unresponsive to stimulus, much like an economy that fails to react to monetary policy.

Motivational speeches, self‑help strategies, and productivity frameworks often operate on the premise that people are rational agents capable of immediate behavioral adjustment. They treat stagnation as a moral failure rather than a systemic one. But when the internal economy of the mind freezes, information cannot circulate. Advice becomes inert. Encouragement feels hollow. The person knows what to do but cannot mobilize the energy to do it. They say, “I know what to do, I just can’t get myself to do it,” or “I want to change, but I feel stuck.” These are not confessions of weakness; they are symptoms of a liquidity crisis. The psychological interest rate has fallen to zero, and no amount of external stimulus can generate movement until confidence and circulation are restored. This failure of traditional motivation reveals a deeper truth about human behavior: change is not driven by information alone but by the availability of emotional and cognitive resources. When those resources are depleted, the system becomes resistant to input. The person is not lazy or indifferent; they are operating within a psychological recession. Their internal market has contracted. The challenge, therefore, is not to push harder but to reintroduce liquidity, to restore the flow of energy, confidence, and expectation that makes action possible.

Recovery begins with micro‑movements rather than macro‑goals. Just as economies recover through small injections of liquidity, individuals recover through small injections of action. A single step, a minor decision, or a brief engagement can begin to thaw the frozen system. Research on habit formation supports this principle: micro‑habits reduce psychological resistance and increase long‑term adherence (Fogg, 2019). The key is not the magnitude of the action but its continuity. Each small movement reintroduces circulation, signaling to the mind that motion is possible again. Over time, these micro‑movements accumulate into momentum, and momentum becomes confidence.

Rebuilding expectational confidence is the next stage of recovery. Expectations are the psychological equivalent of consumer sentiment in economics; they determine whether individuals invest in themselves or withdraw from opportunity. When people experience small wins, their belief in future success strengthens. The mind begins to anticipate positive outcomes rather than fear negative ones. This shift mirrors how consumer confidence boosts economic recovery: optimism fuels spending, and spending fuels growth. In the behavioral economy of the self, optimism fuels effort, and effort fuels transformation. Emotional regulation functions as the stimulus policy of the mind. Techniques such as mindfulness, reframing, and self‑compassion reduce stress and restore cognitive flexibility (Gross, 2015). They lower the psychological cost of action by calming the system and expanding perception. When emotional regulation improves, the mind becomes more responsive to stimuli. It can process information without distortion and make decisions without paralysis. Emotional regulation, therefore, is not a luxury; it is a liquidity mechanism. It keeps the internal economy fluid.

Social support operates as fiscal policy. Supportive relationships inject external resources into a depleted system. They provide encouragement, validation, and shared resilience, all of which increase emotional liquidity. Social connection reduces the cognitive load of stress and buffers against depletion (Cohen & Wills, 1985). In economic terms, it is an infusion of capital from outside the system. In psychological terms, it is the restoration of trust and belonging. When people feel supported, they regain the confidence to act. The presence of others becomes a stabilizing force that prevents further contraction. Reducing loss aversion is another critical intervention. Fear of loss often outweighs the desire for gain, creating a psychological barrier to change. Helping individuals reinterpret risk reduces the emotional weight of potential losses. Behavioral interventions such as reframing and exposure therapy recalibrate fear responses (Beck, 2011). When risk is perceived as manageable rather than catastrophic, the mind becomes willing to invest again, to spend emotional energy on growth. This shift mirrors how investors reenter markets once volatility subsides. The individual, like the economy, begins to move toward expansion.

The behavioral liquidity trap reframes psychological stagnation not as a failure of willpower but as a failure of circulation. It transforms the narrative from “Why am I not trying hard enough?” to “Why is my emotional liquidity low?” This reframing is compassionate and evidence‑based. It aligns with behavioral economic principles that recognize the interplay between confidence, stimulus, and recovery. Human beings, like economies, require confidence to invest, circulation to sustain movement, stimulus to reignite growth, support to stabilize the system, and time to heal. Recovery is not instantaneous; it is cumulative. Each act of movement, each moment of connection, each reframed thought contributes to the restoration of liquidity.

A liquidity trap, whether economic or psychological, is not permanent. With the right stimulus, expectations shift, confidence returns, and movement becomes possible again. The same is true for the human mind. People do not remain stuck because they are weak or unmotivated; they remain stuck because their internal economy has frozen. Emotional liquidity has dried up, expectations have collapsed, and cognitive systems have become risk‑averse. But with micro‑movements, emotional regulation, social support, and renewed expectations, the behavioral liquidity trap can be broken. The mind can move again. And once movement begins, momentum follows.

The path out of stuckness is not paved with grand gestures or sudden breakthroughs. It is built through the quiet restoration of flow, the gradual reintroduction of confidence, flexibility, and hope. When the mind begins to circulate possibilities again, it mirrors the recovery of an economy emerging from recession. The system stabilizes, investment returns, and growth resume. In this way, the behavioral liquidity trap becomes not only a metaphor but a model, a framework for understanding how human beings recover from stagnation and rediscover motion. The mind, like any economy, thrives when its resources flow freely. And when liquidity returns, life begins to move forward once more.

References

1. Beck, J. S. (2011). Cognitive behavior therapy: Basics and beyond. Guilford Press.

2. Cohen, S., & Wills, T. A. (1985). Stress, social support, and the buffering hypothesis. Psychological Bulletin, 98(2), 310–357.

3. Fogg, B. J. (2019). Tiny habits: The small changes that change everything. Houghton Mifflin Harcourt.

4. Gross, J. J. (2015). Emotion regulation: Current Status and future prospects. Psychological Inquiry, 26(1), 1–26.

5. Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–291.

6. Keynes, J. M. (1936). The general theory of employment, interest, and money. Macmillan.

7. Krugman, P. (1998). It’s Back: Japan’s slump and the return of the liquidity trap. Brookings Papers on Economic Activity, 1998(2), 137–205.

8. Loewenstein, G. (2000). Emotions in economic theory and economic behavior. American Economic Review, 90(2), 426–432.

9. Mankiw, N. G. (2019). Principles of economics (9th ed.). Cengage Learning.

10. Schmeichel, B. J., & Baumeister, R. F. (2004). Self‑regulatory strength. Handbook of self‑regulation, 84–98. Seligman, M. E. P. (1975). Helplessness: On depression, development, and death. Freeman.

© 2026 Enoma Ojo. The Behavioral Economy Series. All rights reserved. This work is protected under U.S. and international copyright law. No portion of this series may be copied, stored, or transmitted without written permission from the author, except for brief quotations in critical reviews or academic commentary.