The Economy Within: Understanding the Mind’s Liquidity Trap

The Economy Within: Understanding the Mind’s Liquidity Trap explores one of the most overlooked parallels between macroeconomics and human psychology: the way both systems can become stuck, stagnant, and unresponsive even when resources are available. In economics, a liquidity trap occurs when interest rates fall to near zero, and people still refuse to spend, invest, or take risks. In life, something similar happens inside the mind — moments when opportunities are present, support exists, and the path forward is open, yet a person remains frozen by fear, uncertainty, or emotional exhaustion. This article invites readers to see the liquidity trap not just as a technical economic concept, but as a powerful metaphor for the human experience. It shows how individuals can hoard their potential the same way economies hoard cash: holding back ideas, delaying decisions, avoiding risks, and retreating into psychological safety even when growth is possible. Through this lens, the piece reveals how confidence, expectation, and emotional belief function as the “interest rates” of the mind, invisible forces that determine whether someone moves, invests in themselves, or stays stuck. Blending economic insight with behavioral psychology, the article helps readers recognize the subtle ways fear, scarcity, and uncertainty shape their choices. It offers a deeper understanding of why people sometimes feel immobilized despite having talent, opportunity, or support. And more importantly, it illuminates what it takes to break free: rebuilding trust in the future, restoring internal momentum, and learning to deploy one’s inner resources with intention rather than hesitation. Ultimately, this is an article about reclaiming agency. It shows that just as economies can escape liquidity traps through shifts in confidence and coordinated action, individuals can also unfreeze their inner economy, unlocking creativity, courage, and the willingness to move again.

enoma ojo (2025)

4/3/202615 min read

In macroeconomics, few concepts reveal the limits of monetary policy as sharply as the liquidity trap. It describes a moment when interest rates fall to extremely low levels, sometimes brushing against zero, yet borrowing, spending, and investment refuse to respond. Even when money becomes almost costless, the economy does not stir. Traditional tools lose their force, and policymakers find themselves pushing on a string, unable to convert abundant liquidity into real activity. This is the paradox at the heart of the liquidity trap: the system is not starved of resources; it is saturated with them. What is missing is movement. Households save instead of spending, firms hesitate instead of investing, and financial institutions hold cash instead of lending. The machinery of the economy slows, then stalls, not because it lacks fuel, but because confidence collapses and expectations turn inward. Economists have long studied these episodes, from Japan’s “Lost Decades” to the aftermath of the 2008 financial crisis, moments when monetary stimulus could not overcome the deeper psychological forces shaping behavior. Beneath the charts and policy debates lies a quieter truth: stagnation often begins in the mind before it appears in the market. And this is where the metaphor widens. The liquidity trap is not only an economic condition; it is a human one. Just as nations can become stuck despite abundant resources, individuals can find themselves holding potential they cannot bring themselves to use. The economy within us can freeze in ways that mirror the very systems we build.

A liquidity trap is an economic situation in which monetary policy loses its ability to stimulate growth because interest rates have fallen to extremely low levels, and people still prefer to hold onto cash rather than invest or spend. Even when central banks make borrowing almost costless, households and firms remain cautious, choosing liquidity over risk. As a result, the usual levers of monetary policy, lowering interest rates, expanding the money supply, and encouraging credit, fail to generate meaningful increases in consumption or investment. This creates a paradoxical environment: money is abundant, yet movement is scarce. The financial system becomes saturated with idle funds, and the economy drifts into a state of stagnation that is difficult to escape. Policymakers find themselves with limited tools, watching as fear, uncertainty, and deflationary expectations overpower the incentives they attempt to create.

In essence, a liquidity trap is not simply a technical failure of policy; it is a behavioral freeze. It reveals how deeply economic activity depends on confidence, belief, and the willingness of people to act. When those psychological foundations weaken, even the most aggressive monetary interventions struggle to restore momentum.

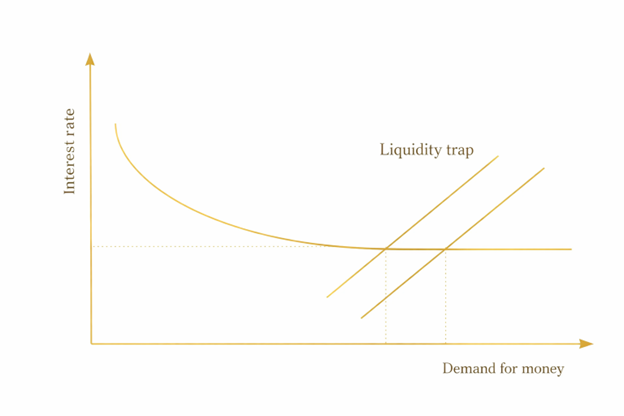

Figure 1: The Liquidity Trap

Source: Author’s Illustration

Figure 1 illustrates how the demand for money behaves when an economy enters a liquidity trap. The downward‑sloping portion of the curve shows the normal relationship between interest rates and money demand: as interest rates fall, people prefer to hold less cash and more interest‑bearing assets. But notice what happens at the bottom of the curve. It flattens out. This flat segment represents the liquidity trap zone, a range where interest rates are already extremely low, and further increases in the money supply no longer push rates down or stimulate spending. In this region, people prefer to hold cash rather than invest, because they expect rates to stay low or fear future economic decline. As a result, Interest rates cannot fall further. Money demand becomes perfectly elastic. Monetary policy loses effectiveness, and the economy becomes stuck in stagnation The upward‑sloping lines intersecting the flat portion show how additional injections of money simply accumulate as idle balances rather than translating into borrowing, lending, or investment. In short, the graph visualizes the core paradox of the liquidity trap: even with abundant money and near‑zero interest rates, economic activity refuses to move.

Simply explained, it is a phenomenon where the trap emerges when economic agents, households, firms, and investors choose to hold onto cash rather than deploy it into productive activity. This behavior is not irrational; it is rooted in fear, uncertainty, and expectations about the future. When people believe that conditions may worsen or that interest rates may rise later, they prefer liquidity over risk. Tversky and Kahneman (1974) argue that the mind defaults to fast, intuitive heuristics when facing uncertainty, and these shortcuts can distort judgment in ways that mirror the irrational movements of financial markets. The result is an economy flooded with money that no one wants to use. Historically, liquidity traps have appeared during periods of deep economic distress. Japan’s “Lost Decades” remain the most cited example: interest rates hovered near zero, central banks injected liquidity, yet investment and consumption remained weak for years. The 2008 global financial crisis and the COVID‑19 economic shock also revealed similar patterns, moments when monetary stimulus could not overcome widespread caution. At the heart of the liquidity trap is a collapse of confidence. Monetary policy assumes that lowering interest rates will encourage people to borrow and spend. But when trust in the future erodes, even free money cannot motivate action. People hoard cash not because they lack opportunities, but because they lack belief. The economy becomes psychologically frozen long before it becomes financially constrained. Bernanke (2000) argues that Japan’s monetary authorities fell into a form of self‑induced paralysis, where fear of making the wrong move became more powerful than the need to make any move at all, a dynamic that mirrors the way individuals freeze when confidence collapses.

This scenario reveals an important truth: economic behavior is deeply intertwined with human psychology. A liquidity trap is not merely a technical failure of policy; it is a behavioral response to fear, uncertainty, and perceived risk. And just as economies can become trapped in liquidity, so can individuals. The same forces that cause investors to hoard cash can cause people to hoard their potential, their ideas, and their decisions. In the economy, a liquidity trap begins when interest rates fall, and money refuses to move. In the mind, it begins when confidence falls, and potential refuses to act. The parallels are striking: both systems become saturated with resources yet paralyzed by fear. The individual, like the investor, hoards safety. The mind, like the market, waits for a signal that never comes. And just as monetary policy loses its power in a liquidity trap, so too do encouragement, opportunity, and support lose their power when the psyche is frozen. The trap is not technical; it is emotional.

In a hypothetical economy, it can become saturated with idle money, and individuals can become flooded with idle potential. In both cases, the problem is not scarcity; it is stagnation. The liquidity trap, in its economic form, reveals what happens when fear and uncertainty override incentive. But this trap is not confined to markets. It exists within minds. When confidence collapses, when fear rises, when expectations turn inward, the human psyche mirrors the same paralysis. The tools of motivation, like the tools of monetary policy, lose their power. And so begins the psychology of the liquidity trap: a state where the mind hoards possibility but refuses to act. Just as an economy can become saturated with idle money, a person can become saturated with idle potential. Ideas accumulate. Dreams accumulate. Skills accumulate. But none of them convert into action. The individual is not lacking capacity; they are lacking psychological movement. The internal interest rate, the perceived reward for taking a step, falls so low that even meaningful opportunities feel unworthy of effort. The mind enters its own liquidity trap: full of resources, yet unable to deploy them. A psychological liquidity trap occurs when a person becomes so overwhelmed by fear, doubt, or instability that they stop acting, even when the cost of action is low and the potential benefit is high. They hoard energy, ideas, and decisions the same way investors hoard cash. Akerlof and Shiller (2009) argue that economic outcomes are shaped not only by rational calculations but by the psychological forces, confidence, fear, narratives, and expectations that determine whether individuals and societies choose to act at all.

In macroeconomics, interest rates represent the cost of borrowing. In psychology, fear represents the cost of trying. When fear rises, the “interest rate” on action becomes too high. Even when the external world lowers the cost, new opportunities, encouragement, and support, the internal rate remains elevated. The person hoards safety the way investors hoard cash. They wait for a “better moment,” a “clearer signal,” a “safer future.” But that future never arrives, because fear keeps the internal rate above zero. Keynes argued that expectations about the future shape economic behavior more than present conditions. The same is true for individuals. People often stop themselves long before the world stops them. They imagine failure before they attempt success. They anticipate rejection before they speak. They forecast disappointment before they begin. The psychological liquidity trap is not caused by a lack of opportunity; it is caused by a lack of belief in what opportunity could become.

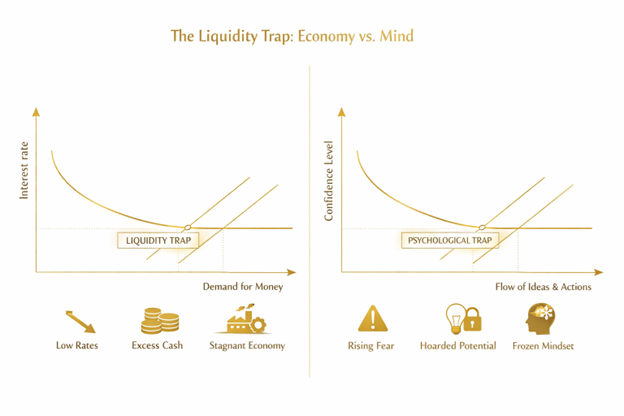

Figure 2: The Liquidity Trap and The Human Mind

Source: Author’s Illustration

In Figure 2, we see the classic liquidity trap in macroeconomics. As interest rates fall, the demand for money typically rises, but in extreme cases, this relationship breaks down. The curve flattens, signaling that even near-zero interest rates fail to stimulate borrowing or investment. The economy becomes saturated with cash, yet remains stagnant. Icons below the graph reinforce this dynamic: low rates, excess cash, and a stalled economic engine. On the right side of the diagram, it mirrors the economic paralysis with a psychological counterpart. Here, the vertical axis represents confidence, and the horizontal axis tracks the flow of ideas and actions. As confidence declines, the mind’s willingness to act diminishes. Eventually, the curve flattens, just like in the economic model, indicating a state where fear overrides potential. The icons below capture this internal freeze: rising fear, hoarded potential, and a frozen mindset.

Pairing these diagrams, we invite readers to see liquidity traps not just as technical failures, but as behavioral phenomena. It challenges us to ask: where in our lives are we hoarding potential? Where has fear flattened our curve? By visualizing the economy and the mind side by side, the infographic becomes more than a teaching tool; it becomes a mirror. And in that reflection, the path to restoration begins with confidence, belief, and the courage to circulate again. This paired visual invites us to see the liquidity trap not just as an economic anomaly but as a metaphor for human behavior. It asks where we, too, may be holding onto excess “liquidity”, ideas, talents, decisions, without deploying them. It challenges us to recognize that stagnation is often psychological before it becomes practical. And it suggests that escape begins not with more resources, but with restored confidence, renewed belief, and the courage to circulate possibility again.

This internal freeze is not caused by laziness or lack of ambition. It is caused by a collapse of confidence. When the mind no longer trusts the environment, it defaults to safety. It holds back. It waits. It preserves rather than invests. In economics, liquidity traps arise when people expect future interest rates to rise or when they distrust the system. In psychology, the same pattern appears in people who delay decisions because they expect future conditions to be better, or because they distrust their current environment. The result is stagnation. Not because opportunities are absent, but because the mind refuses to engage with them. The person becomes mentally conservative, emotionally risk‑averse, and behaviorally frozen. Fear of loss is one of the strongest drivers of this internal trap. Behavioral economics has long shown that humans feel the pain of losing far more intensely than the pleasure of gaining. When fear dominates, even zero‑cost opportunities feel expensive.

Cognitive overload also plays a role. When the brain is overwhelmed by too many decisions, too many uncertainties, or too many threats, it shuts down higher‑order thinking. The safest option becomes inaction. The mind hoards its limited cognitive resources. Scarcity mindset deepens the trap. When people feel they don’t have enough time, money, energy, or support, they cling tightly to whatever they have left. They avoid risks. They avoid change. They avoid anything that feels like an investment. Over time, this scarcity becomes self‑reinforcing. The more a person holds back, the more stagnant they feel. The more stagnant they feel, the more they hold back. The psychological liquidity trap becomes a loop. Learned helplessness is another contributor. When individuals experience repeated failures, instability, or unpredictability, they begin to believe that their actions no longer matter. Even when conditions improve, they remain frozen. This is why people stay in jobs they dislike, relationships that drain them, or environments that limit them. The trap is not external, it is internal. The mind has stopped believing that investment leads to return.

At the societal level, liquidity traps appear in communities where trust is low, corruption is high, or institutions are weak. People avoid risks because the system feels unsafe. Innovation slows. Creativity declines. Progress stalls. In workplaces, the same dynamic emerges. When employees feel micromanaged, undervalued, or unsupported, they stop offering ideas. They stop taking initiative. They stop investing their discretionary effort. They hoard their potential. In families, psychological liquidity traps show up as emotional withdrawal. When communication feels unsafe or unpredictable, people stop sharing. They stop expressing. They stop engaging. They hold their emotions like cash under a mattress. The symptoms of a psychological liquidity trap are subtle but powerful. Overthinking replaces action. Procrastination replaces momentum. Comfort zones replace growth. The person becomes a spectator in their own life. Creativity declines because creativity requires risk. Decision‑making slows because decisions require confidence. Opportunities pass by because opportunities require movement. The person becomes mentally liquid but behaviorally frozen. Eggertsson and Krugman (2012) argue that severe debt overhang forces households and firms into aggressive deleveraging, which depresses demand so sharply that even zero interest rates cannot restore economic momentum, creating a classic liquidity trap.

In a liquidity trap, holding cash feels safe but ultimately harms the economy. In life, holding back feels safe but ultimately harms the self. The paradox is that the very instinct meant to protect us, caution, becomes the force that traps us. The more we cling to safety, the more stagnant we become. The more stagnant we become, the more dangerous the movement feels. The trap tightens not because the world is hostile, but because the mind has stopped circulating courage. Economies escape liquidity traps not through more money, but through restored confidence. The same is true for individuals. Movement begins when belief returns, not belief in perfection, but belief in possibility. Confidence is the psychological equivalent of monetary stimulus: it increases the willingness to act, to risk, to invest in one’s own future. Once confidence rises, even small steps create momentum. The mind begins to circulate again. Escaping this trap requires more than motivation. It requires rebuilding confidence, the psychological equivalent of restoring trust in an economy. Small wins matter. They create momentum. They signal safety. They restore belief. Reducing perceived risk is also essential. Clarity reduces fear. Structure reduces uncertainty. When people understand the path ahead, they are more willing to take the first step. Psychological safety is the foundation. Humans move when they feel safe. They invest when they feel supported. They take risks when they believe the environment will not punish them for trying. External intervention can help. Just as governments use fiscal stimulus to break economic stagnation, people often need encouragement, accountability, or support to break psychological stagnation. Sometimes the mind needs a nudge.

Reframing the future is another powerful tool. When the future feels bleak, the present becomes a place to hide. But when the future feels possible, the present becomes a place to prepare. Hope is an internal stimulus. The key insight is that stagnation is rarely about the absence of opportunity. It is about the absence of confidence. People do not freeze because they lack options. They freeze because they lack belief. The liquidity trap teaches us that incentives alone are not enough. You can lower the cost of action, but if fear remains high, nothing changes. The mind will continue to hoard its potential. To escape the trap, economically or psychologically, people must first believe that the future is worth investing in. When confidence returns, movement returns. When trust returns, investment returns. And when

In the end, the liquidity trap, whether in an economy or within a human life, reveals a simple but profound truth: movement does not begin with resources; it begins with belief. Nations can inject capital, and individuals can accumulate knowledge, opportunities, and support, yet nothing changes until confidence returns. The mind, like the market, waits for a signal that the future is safe enough to step toward. But here is the quiet power we often overlook: the first signal does not have to come from the world. It can come from within. A single act of courage, a small decision to deploy one’s potential rather than hoard it, can break the psychological stasis. Just as economies escape liquidity traps through expectations, through the belief that tomorrow can be different, so do people.

When we choose movement over fear, even in microscopic ways, we restore the internal circulation of possibility. We remind ourselves that potential is not meant to sit idle, that ideas are not meant to be stored, and that the self is not meant to be frozen by uncertainty. The economy within us begins to recover the moment we do. And once confidence returns, once belief rises even slightly, the mind, like any revitalized market, discovers that it was never empty. It was simply waiting for permission to move again. Belief returns, and the economy begins to grow again.

At the beginning of this article, we entered the mind the way an economist enters a stalled market, listening for the faint buzz of circulation, searching for the places where energy once moved freely. And now, at the end, we return to that same interior landscape, but with a different kind of seeing. We understand that the stillness was never emptiness; it was potentially held in suspension, waiting for a shift in expectation, a softening of fear, a single brave signal that tomorrow might be worth investing in. We should note that the liquidity trap within us is not a flaw but a pause, a moment when the psyche gathers itself, uncertain of the world’s promises, cautious about deploying its reserves. Yet even the most stagnant economy stirs when belief returns, and so does the human spirit. Confidence, once rekindled, moves through the mind like warmth through cold metal, loosening what was rigid, awakening what was dormant. As we step out of this exploration with a quieter kind of power. We know now that the mind does not need a dramatic rescue or a sudden windfall. It needs only the smallest act of release, the willingness to let one thought, one hope, one intention flow again. That is enough to break the stasis. That is enough to begin recovery.

In this way, the economy within us mirrors every economy we have ever studied: it responds not to force, but to faith; not to abundance, but to the courage to use what we already possess. We often imagine that transformation requires a dramatic influx of resources, more time, more clarity, more certainty, more strength. But systems rarely change because they are flooded with new inputs. They change because something inside them begins to move again. Confidence is the first currency of renewal. It is the quiet signal that tells a stagnant system it is safe to circulate, safe to risk, safe to release what has been held in reserve. And just as a national economy can shift when expectations shift, when people believe growth is possible, the internal economy awakens when we dare to believe that our next step is worth taking.

This is the paradox at the heart of every liquidity trap, internal or external: the resources are present, but the will to deploy them is frozen. The mind hoards its potential the way a frightened market hoards its cash, not because it lacks value, but because it doubts the future. And yet the moment we choose movement, even the smallest movement, the entire system begins to recalibrate. A single decision becomes a signal. A signal becomes momentum. Momentum becomes recovery. The shift does not begin with abundance. It begins with permission, the permission we give ourselves to act before we feel fully ready, to invest before certainty arrives, to trust that motion itself will reveal the path when we choose to move, even slightly, the entire system shifts. The mind warms. Possibility circulates. The self begins to expand into the space it once feared. And in that moment, we discover the truth economists have always known but rarely name: no system is transformed by pressure alone. It is transformed by belief, the belief that what we hold is enough to begin, and that beginning is enough to change everything.

AI tools were used to support the Infographics and Images, and the editing of this article. All ideas, interpretations, and final decisions reflect the author’s independent judgment.

References:

1. Akerlof, G. A., & Shiller, R. J. (2009). Animal spirits: How human psychology drives the economy, and why it matters for global capitalism. Princeton University Press.

2. Bernanke, B. S. (2000). Japanese monetary policy: A case of self‑induced paralysis? In R. Mikitani & A. Posen (Eds.), Japan’s financial crisis and its parallels to U.S. experience (pp. 149–166). Institute for International Economics.

3. Blanchard, O. (2017). Macroeconomics (7th ed.). Pearson.

4. Eggertsson, G. B., & Krugman, P. (2012). Debt, deleveraging, and the liquidity trap: A Fisher‑Minsky‑Koo approach. Quarterly Journal of Economics, 127(3), 1469–1513.

5. Friedman, M. (1968). The role of monetary policy. American Economic Review, 58(1), 1–17.

6. Kahneman, D. (2011). Thinking, fast and slow. Farrar, Straus and Giroux.

7. Keynes, J. M. (1936). The general theory of employment, interest and money. Macmillan.

8. Krugman, P. (1998). It’s Back: Japan’s slump and the return of the liquidity trap. Brookings Papers on Economic Activity, 1998(2), 137–205.

9. Laibson, D. (1997). Golden eggs and hyperbolic discounting. Quarterly Journal of Economics, 112(2), 443–477.

10. Mankiw, N. G. (2021). Principles of economics (9th ed.). Cengage Learning.

11. Mishkin, F. S. (2019). The economics of money, banking, and financial markets (12th ed.). Pearson.

12. Phelps, E. S. (2013). Mass flourishing: How grassroots innovation created jobs, challenges, and change. Princeton University Press.

13. Shiller, R. J. (2019). Narrative economics: How stories go viral and drive major economic events. Princeton University Press.

14. Thaler, R. H., & Sunstein, C. R. (2008). Nudge: Improving decisions about health, wealth, and happiness. Yale University Press.

15. Tversky, A., & Kahneman, D. (1974). Judgment under uncertainty: Heuristics and biases. Science, 185(4157), 1124–1131.

© 2026 Enoma Ojo. All rights reserved.

No part of this article may be reproduced, distributed, or transmitted in any form without prior written permission from the author